Unearned Revenue

This changes if advance payments are made for services or goods due to be provided 12 months or more after the payment date. In such cases, the unearned revenue will appear as a long-term liability on the balance sheet.

Accrued liabilities are adjusted and recognized on the balance sheet at the end of each accounting period; adjustments are used to document goods and services that have been delivered but not yet billed. Under the expense recognition principles of accrual accounting, expenses are recorded in the period in which they were incurred and not paid. If a company incurs an expense in one period but will not pay the expense until the following period, the expense is recorded as a liability on the company’s balance sheet in the form of an accrued expense. When the expense is paid, it reduces the accrued expense account on the balance sheet and also reduces the cash account on the balance sheet by the same amount.

Unearned Revenue Journal Entry

That can give the impression that the company’s revenue is “lumpy,” meaning it goes long periods without earning any money at all. Accounts receivable are invoices the business has issued to customers that have not been paid yet. Accrued revenue represents money the business has earned but has not yet invoiced to the customer. By contrast, imagine a business gets a $500 invoice for office supplies. When the AP department receives the invoice, it records a $500 debit in the accounts payable field and a $500 credit to office supply expense.

Unearned Revenue

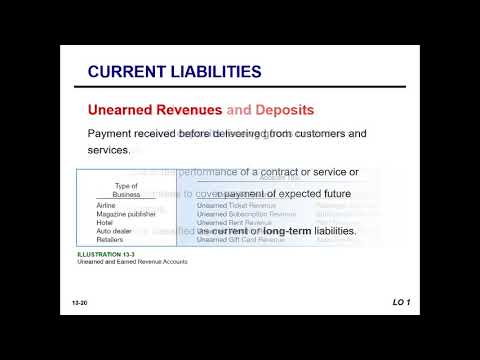

Unearned revenue is great for a small business’s cash flow as the business now has the cash required to pay for any expenses related to the project in the future, according to Accounting Tools. Current liabilities are financial obligations of a business entity that are due and payable within a year. A liability occurs when a company has undergone a transaction that has generated an expectation for a future outflow of cash or other economic resources. Accounting reporting principles state that unearned revenue is a liability for a company that has received payment (thus creating a liability) but which has not yet completed work or delivered goods. The rationale behind this is that despite the company receiving payment from a customer, it still owes the delivery of a product or service.

As the prepaid service or product is gradually delivered over time, it is recognized as revenue on theincome statement. Because the company actually incurred 12 months’ worth of salary expenses, an adjusting journal entry is recorded at the end of the accounting period for the last month’s expense. The adjusting entry will be dated December 31 and will have a debit to the salary expenses account on the income statement and a credit to the salaries payable account on the balance sheet. Accrued liabilities are usually expenses that have been incurred by a company as of the end of an accounting period, but the amounts have not yet been paid or recorded in the general ledger.

So, a prepaid account will always be represented on the balance sheet as an asset or a liability. When the prepaid is reduced, the expense is recorded on the income statement. While prepaids and expenses are related, they are distinctly different. Accounting for prepaid rent doesn’t have to be complicated, but it does require attention at month-end-close. In a basic general ledger system, an accountant or bookkeeper records a prepaid asset to a balance sheet account.

At the end of the first quarter of 2019, Morningstar had $233 million in unearned revenue, up from $195.8 million from the prior year period. The company classifies the revenue as ashort-term liability, meaning it expects the amount to be paid over one year.

A liability account that reports amounts received in advance of providing goods or services. When the goods or services are provided, this account balance is decreased and a revenue account is increased. Accruals are revenues earned or https://www.bookstime.com/articles/is-unearned-revenue-a-current-liability expenses incurred which impact a company’s net income, although cash has not yet exchanged hands. Accounts receivable is the balance of money due to a firm for goods or services delivered or used but not yet paid for by customers.

When reviewing this line item, it’s important to substantiate the balance with source documents. This could include bank statements, billing statements and other documentation, to assure the prepaid balance is complete and accurate. Looking for training on the income statement, balance sheet, and statement of cash flows? At some point managers need to understand the statements and how you affect the numbers. Learn more about financial ratios and how they help you understand financial statements.

- When reviewing this line item, it’s important to substantiate the balance with source documents.

- The accrued revenue and accounts receivable entries in accrual accounting allow the company to recognize revenue and place it on the balance sheet as it earns the money.

- A liability is recorded when a company receives a prepayment of rent from a tenant or a third-party.

- Once the product or service is delivered, unearned revenue becomes revenue on the income statement.

- This is advantageous from a cash flow perspective for the seller, who now has the cash to perform the required services.

- At the end of 12 months all the unearned service revenue (unearned) will have been taken to the service revenue account (earned).

At the end of the month, the owner debits unearned revenue $400 and credits revenue $400. He does so until the three months is up and he’s accounted for the entire $1200 in income both collected and earned out.

It can be classified as a long-term liability if performance is not expected within the next 12 months. Unearned revenue is a current liability and is commonly found on the balance sheet of companies belonging to many industries. because the obligation is typically fulfilled within a period of less than a year.

While the interest fees for December, January, February and March all come at once, this $2,000 payment actually comprises four $500 installments of accrued unearned revenue liability revenue. Corporate accountants keep track of myriad types of revenue that flows through companies, most of which bear enigmatic or even misleading names.

The earned revenue is recognized with an adjusting journal entry called an accrual. The revenue recognition principle dictates the process and timing by which revenue is recorded and recognized as an item in a company’s financial statements. Theoretically, there are multiple points in time at which revenue could be recognized by companies. Image from AmazonBalance Sheet – Check out CFI’s Advanced Financial Modeling & Valuation Course for an in-depth valuation of Amazon.

This process is repeated as many times as necessary to recognize rent expense in the proper accounting period. Prepaid rent is recorded as an asset when an organization makes a prepayment of rent to a landlord or a third-party. A liability is recorded when a company receives a prepayment of rent from a tenant or a third-party. It is important for accountants, business owners and managers to understand this distinction. Failure to classify prepaids accurately on the balance sheet can lead to material misstatements of financial information and poor business decision-making.

Proper recording and amortization of prepaids is important for producing accurate, reliable financial statements. Accrued revenue is capital not yet received during a fiscal period for services already rendered. It usually assumes the form of interest or future payments due on items sold on credit or installment plans. For instance, assume your company provides a loan valued at $10,000 in December with a repayment date the following March and a total of $2,000 interest. The recipient of the loan pays you the full value of the loan in March, including interest.

This approach helps highlight how much sales are contributing to long-term growth and profitability. These account balances do not roll over into the next period after closing. https://www.bookstime.com/ The closing process reduces revenue, expense, and dividends account balances (temporary accounts) to zero so they are ready to receive data for the next accounting period.

Accrued revenue and unearned revenue, two types of capital common on company ledgers, count amongst these many revenue streams. Stark contrasts exist between these types of capital; enough so that in a very basic way accrued revenue constitutes the opposite of unearned revenue.

A company pays its employees’ salaries on the first day of the following month for services received in the prior month. If on December 31, the company’s income statement recognizes only the salary payments that have been made, the accrued expenses from the employees’ services for December will be omitted. An example of an accrued expense is when a company purchases supplies from a vendor but has not yet received an invoice for the purchase. Employee commissions, wages, and bonuses are accrued in the period they occur although the actual payment is made in the following period. As each month passes, one rent payment is credited from the prepaid rent asset account, and a rent expense account is debited.